Debt is not always a moral failure. Life is more complicated than that. Men borrow money for homes, vehicles, medical emergencies, education, business, family obligations, and seasons where the math simply does not work any other way. Pretending all debt is the same is lazy advice, and lazy advice does not help anyone build a better life.

But debt is never neutral.

Every debt creates a claim on your future. It reaches forward, grabs part of money you have not earned yet, and assigns it to a decision already made. Sometimes that decision was necessary. Sometimes it was strategic. Sometimes it was careless. Sometimes it was emotional. But either way, the payment remains.

That is why debt belongs in the conversation around Tenet 4: Financial Maturity. Financial maturity is not about becoming rich, looking successful, or turning every dollar into a personal virtue contest. It is about staying free. And few things quietly reduce freedom faster than obligations you can no longer escape.

Debt Rarely Feels Like a Trap at First

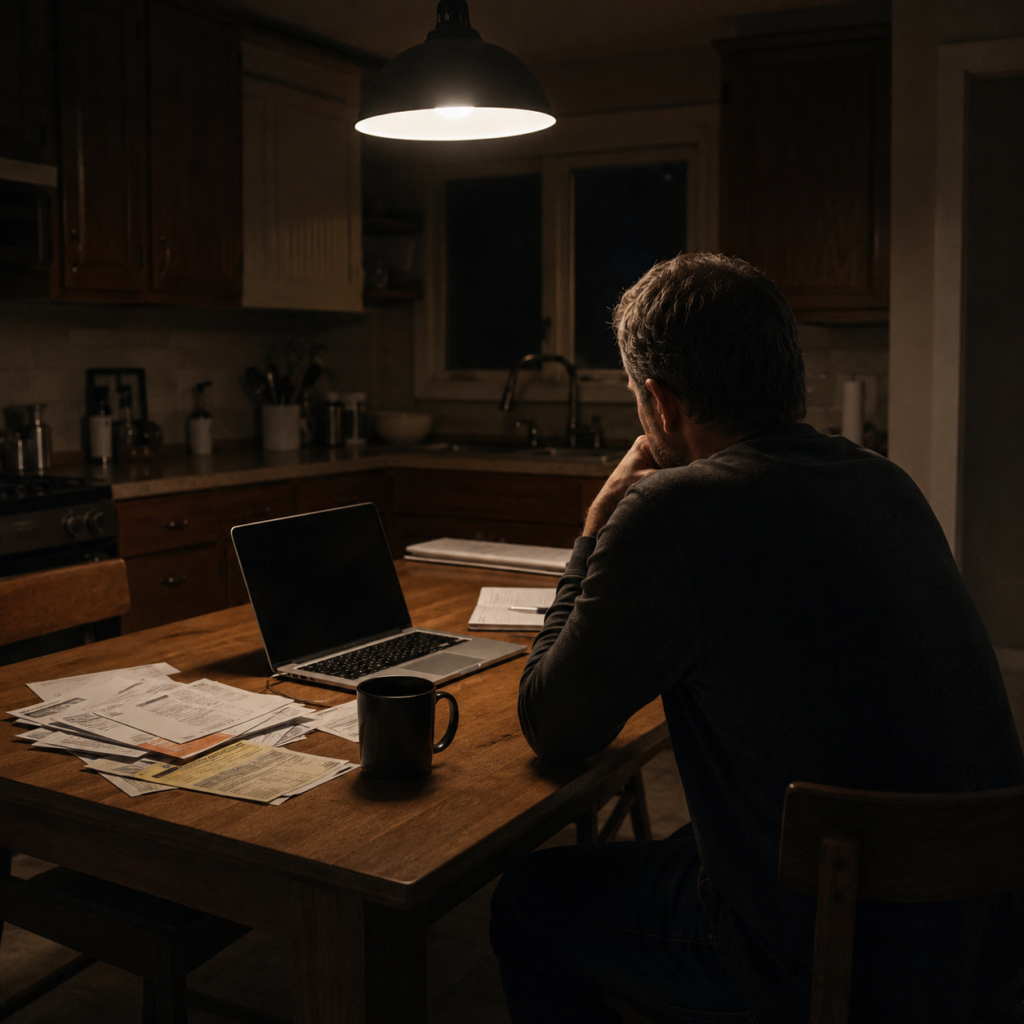

Most debt does not announce itself as a trap.

It usually arrives dressed as a solution.

The old car is unreliable, so the new payment feels reasonable. The family needs a break, so the vacation goes on the card “just this once.” The house needs repairs, the kid needs help, the business needs equipment, the furnace dies, the dog swallows something expensive, the medical bill arrives, or the month simply has more problems than money.

Other times, debt feels less practical and more emotional. A man may finance something because he is tired of feeling behind. He may upgrade because the old version makes him feel small. He may spend because he has worked hard and wants evidence that all that effort has produced something visible. He may call it a reward, a necessity, or an investment in his happiness.

Sometimes he may even be right.

That is the problem. Debt can be reasonable enough in the moment that it becomes hard to judge honestly. One payment seems manageable. One balance does not look dangerous. One extra obligation feels like the cost of being an adult.

But debt becomes dangerous through accumulation and repetition. The individual decisions may be explainable. The pattern is what eventually closes in.

A man does not wake up one morning and decide to surrender his freedom. More often, he gives it away in monthly payments.

The Payment Is Only Part of the Cost

The obvious cost of debt is the money. Interest, fees, minimum payments, longer terms, late charges, penalties, and the slow insult of paying more for something because you did not have the cash when you needed or wanted it.

But that is not the whole cost.

Debt also carries mental load. It sits in the background. It makes every paycheck feel partially spoken for before it arrives. It changes the way a man looks at work, risk, conflict, and time. He may still function. He may still show up. He may still provide. But the space inside his life gets smaller.

That shrinking space matters.

A man with heavy payments may stay in a job long after the work has become corrosive because he cannot afford a gap. He may avoid starting something better because the risk feels impossible. He may postpone necessary medical care, delay hard conversations, or tolerate disrespect because the household budget has no room for disruption.

Debt does not always shout.

Sometimes it whispers, “You cannot afford to move.”

Debt Changes the Meaning of a Paycheck

There is a difference between earning money and owning your income.

A paycheck can look decent on paper while very little of it actually belongs to the man receiving it. The mortgage or rent takes its portion first. The vehicle payment follows. Then credit cards, loans, insurance, utilities, subscriptions, past decisions, and the ordinary costs of staying alive.

By the time the paycheck lands, much of it may already be gone in practical terms.

That is when income becomes less like opportunity and more like maintenance. The man is not building. He is servicing. He is feeding the machine that allows him to keep living the way he has already committed to living.

Some of that is unavoidable. Everyone has obligations. Adult life costs money, and pretending otherwise is useless. But financial maturity requires a man to notice when his income is no longer creating options. If every raise disappears into lifestyle, if every bonus goes toward catching up, if every month depends on nothing going wrong, then the issue is not just how much he makes.

The issue is how much of his future has already been sold.

The Hardest Debt to Admit Is Status Debt

Some debt comes from survival. Some comes from timing. Some comes from lack of options. Those deserve honesty, not contempt.

Status debt is different.

Status debt is money borrowed to support an image. It is the vehicle that says something the bank account cannot support. It is the trip taken mostly because everyone is exhausted and nobody wants to admit the household needs rest more than scenery. It is the furniture, gear, clothes, tools, toys, home upgrades, gadgets, and lifestyle signals bought less for utility than for emotional relief.

That does not make the man evil. It makes him human.

Men are not immune to insecurity. They just tend to dress it differently. A man may not say, “I feel behind and need to prove I am doing well.” He may say, “I needed a reliable truck.” Maybe he did. But did he need that truck? That trim package? That payment? That debt term? That insurance cost? That much pressure attached to transportation?

Those are adult questions.

Financial maturity does not demand that a man live cheaply forever. It does demand that he stop confusing identity with affordability. There is a deep difference between buying something useful and borrowing money to feel like a version of yourself you have not actually built yet.

Status debt is expensive because it charges interest on insecurity.

Survival Debt Deserves a Different Conversation

It is important not to flatten this topic into a scolding lecture.

Some men are carrying debt because life hit them hard. Medical bills. Divorce. Job loss. A sick child. Aging parents. A failed business. A necessary relocation. A major repair that could not wait. A season of underemployment. Inflation pressing against wages that did not keep up.

That kind of debt needs a different tone.

A man who borrowed to survive does not need shame added to the balance. He needs clarity, a plan, and a way back toward room. Shame tends to make debt worse because it drives avoidance. Avoidance leads to missed statements, late fees, silence, defensiveness, and the kind of hopelessness that turns a difficult situation into a permanent identity.

The mature question is not, “How do I punish myself for being here?”

The mature question is, “What does the current reality require now?”

That may mean cutting spending. It may mean calling creditors. It may mean consolidating carefully, not desperately. It may mean increasing income, selling something, downsizing, renegotiating expectations, or having the uncomfortable conversation that everyone in the household has been circling for months.

The path out may be slow. That does not make it fake.

A slow plan is still a plan.

Debt Makes Men Tolerate Things They Should Be Able to Leave

This is one of the least discussed parts of debt.

Debt can make a man stay.

Stay in a job where he is treated poorly. Stay in a business partnership that no longer works. Stay in a town he needs to leave. Stay in a lifestyle that looks fine from the outside but feels like a cage from the inside. Stay quiet in conversations where he should be honest because any disruption might threaten the fragile financial arrangement holding everything together.

Freedom is not only the ability to buy what you want.

Freedom is the ability to stop participating in what is damaging you.

That kind of freedom requires margin. Not endless wealth. Not luxury. Just enough room that every decision is not made under threat.

A man with no margin becomes easier to control. Employers know it. Lenders know it. Advertisers know it. Sometimes family systems know it too, even if nobody says it out loud.

Debt narrows the space between discomfort and obedience.

That is why reducing debt is not just a financial act. It can become a personal act of reclaiming authority over your own life.

The Family Cost of Debt

Debt rarely affects only the person whose name is on the account.

In a household, financial pressure becomes weather. Everyone feels it, even when the numbers are not discussed openly. Children may not understand the payment schedule, but they can sense tension. A spouse may not know every balance, but they usually know when money has become a topic to avoid. Conversations become shorter. Patience thins. Small expenses start sounding like accusations.

This is where financial maturity becomes relational.

Money secrecy corrodes trust. So does financial recklessness. So does one person carrying all the worry while the other gets to remain comfortably vague. In many households, the debt itself is not the only source of damage. The silence around it does just as much harm.

A man does not need to be perfect with money to lead well. But he does need to be honest.

Leadership in this area may look like sitting down with the numbers when he would rather do almost anything else. It may look like admitting the situation is tighter than he wanted. It may look like apologizing for choices that added pressure. It may look like asking for partnership instead of pretending control.

That is not weakness.

That is adulthood.

The Debt Spiral Usually Has a Story

Most debt spirals are not only mathematical. They have a story behind them.

“I work hard, so I deserve this.”

“We’ll catch up next month.”

“It’s only the minimum payment.”

“This is normal.”

“Everyone has car payments.”

“We needed a break.”

“It will be fine once the raise comes.”

“I don’t want my family to feel limited.”

Some of those statements may contain truth. That is what makes them useful as excuses. A good excuse usually has enough truth in it to avoid immediate collapse.

But stories can become dangerous when they protect patterns that are no longer working.

One of the marks of financial maturity is the ability to challenge your own story without collapsing into self-hatred. Maybe you did work hard. Maybe you did need rest. Maybe your family did deserve something good. Maybe the emergency was real. Maybe the purchase made sense at the time.

And maybe the pattern still has to change.

Both can be true.

Getting Out Requires Less Drama Than People Think

Debt reduction is often sold with too much intensity. Extreme sacrifice. No fun. Total austerity. Sell everything. Never drink coffee again. Live like a monk until the balance hits zero.

That approach may work for some people. It also burns people out.

A more durable approach starts with clarity and repetition. List the debts. Know the rates. Know the minimums. Know which balances are expensive, which are manageable, and which are emotionally noisy but mathematically less urgent. Stop adding new lifestyle debt. Build a small emergency buffer so the next flat tire does not go straight back onto the card. Then attack the debt with consistency.

There are different methods. Some people prefer paying the smallest balances first because early wins build momentum. Others prefer attacking the highest-interest debt because the math is cleaner. The best method is usually the one a man will actually follow long enough to matter.

This is where Tenet 15: Legacy of Repeated Actions becomes relevant. Financial freedom does not usually arrive through one heroic gesture. It comes from repeated decisions that gradually change what is normal.

Make the payment.

Do not add the new balance.

Wait before buying.

Tell the truth sooner.

Repeat.

Not glamorous. Effective.

You Do Not Need to Hate Debt to Respect Its Power

A mature man does not need a cartoonish view of debt.

He does not need to pretend all borrowing is evil. He does not need to shame men who are doing their best under pressure. He does not need to turn financial discipline into a personality disorder.

He does need to respect debt’s power.

Debt can be a tool, but it is a tool with teeth. Used carefully, it may help acquire a home, build a business, navigate an emergency, or bridge a season. Used casually, it can turn income into maintenance, comfort into pressure, and ambition into obligation.

The question is not simply, “Can I afford the payment?”

That is the lender’s question.

The better question is, “What does this payment do to my freedom?”

Does it reduce options? Does it increase stress? Does it weaken the household? Does it delay a more important goal? Does it serve something real, or does it mainly protect an image?

Those questions are slower than desire. That is why they work.

Freedom Is Built by Taking Back the Future

Reducing debt is not about becoming morally superior. It is about taking back pieces of your future that were already spoken for.

Every balance lowered gives tomorrow a little more room. Every payment eliminated returns a piece of income to your control. Every avoided impulse purchase keeps your future from being drafted into service by your present mood. Every honest conversation reduces the power of avoidance.

This is not dramatic work, but it is serious work.

A man who reduces debt becomes harder to corner. He has more room to change jobs, handle emergencies, support people he loves, take calculated risks, and say no without immediate fear. He does not become invincible. He becomes less fragile.

That is the point.

Financial maturity is not about hating money, worshiping money, or proving yourself through money. It is about using money in a way that supports responsibility, stability, and freedom.

Debt quietly reduces freedom when it is ignored, normalized, or used to protect appearances.

Freedom comes back the same way it was lost.

One decision at a time.

Where to Go Next

This page is part of Tenet 4: Financial Maturity, which is about owning your future without turning money into a measure of human worth.

Continue with:

Living Within Your Means Without Living Small

Emergency Funds Are Not Paranoia

The Difference Between a Financial Goal and a Financial Fantasy

Tenet 15: Legacy of Repeated Actions

Continue Through the 15 Tenets

Back to Tenet 4: Financial Maturity: Owning Your Future

All Tenets: 15 Tenets for Positive Masculinity

Next Tenet: Tenet 5: Family First