Saving money is good.

That should not be controversial, but modern life keeps trying to sell grown men things they do not need with money they do not have so they can impress people who are mostly looking at their own phones.

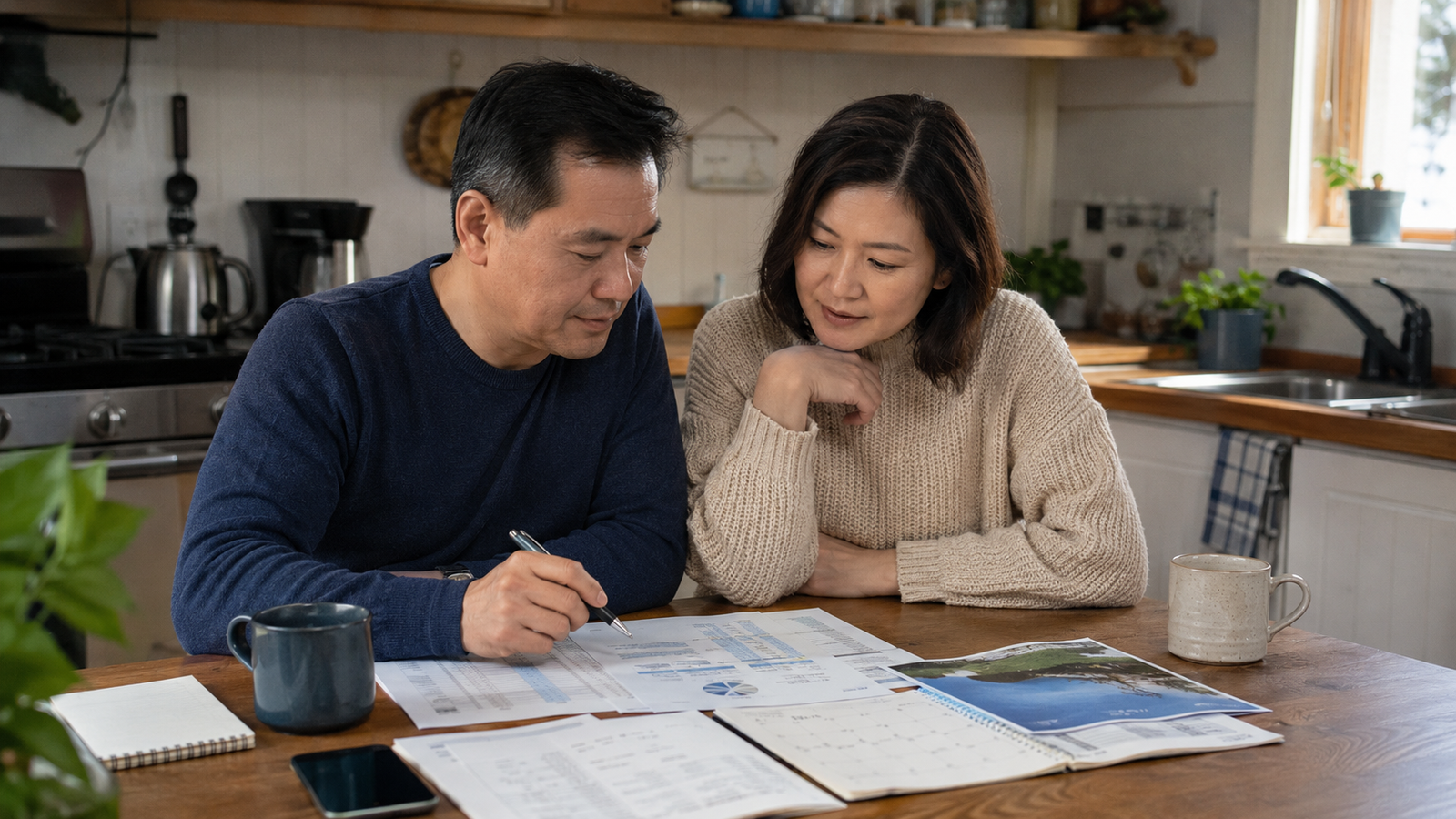

A man should save. He should plan. He should understand that debt can quietly reduce freedom. He should know that emergencies are not unusual events invented by pessimists. Cars break, roofs leak, jobs change, bodies age, and the refrigerator has an instinct for dying during expensive months.

Financial discipline matters.

But saving can become distorted too.

A man can become so focused on protecting the future that he treats the present like a waiting room. He can begin to see every meal out, trip, gift, repair, hobby, family experience, or small comfort as an enemy of the spreadsheet.

That is not always wisdom.

Sometimes it is fear with a brokerage account.

This page supports Tenet 1: Strength Through Balance. It also connects directly to Tenet 4: Financial Maturity, where the deeper work of debt, emergency savings, goals, income, and financial responsibility belongs.

Tenet 4 asks whether a man handles money responsibly. Tenet 1 asks whether money has remained in proportion to the rest of his life.

Money Is a Tool, Not a Shrine

Money matters because life is not free.

Housing costs money. Food costs money. Health costs money. Transportation, children, repairs, aging parents, taxes, mistakes, and apparently doing absolutely nothing all cost money.

A man who ignores money is not necessarily spiritual, relaxed, or above materialism. He may simply be handing the consequences to his family, his creditors, or the older version of himself who will have fewer years available to repair the damage.

Money is a serious tool. It helps create shelter, stability, options, generosity, health, independence, and the ability to leave situations that would otherwise own a man.

But it is still a tool.

It should serve the life. The life should not be reduced to protecting the money.

Save enough to protect the future. Spend enough to honor the present. Let neither fear nor impulse run the house.

Money Can Control a Man in Two Directions

The man who cannot stop spending and the man who cannot allow himself to spend may look like opposites.

Both can be ruled by money.

One spends to chase pleasure, status, relief, or approval. The other saves to chase certainty, control, or protection from every possible future discomfort.

One says, “I deserve this,” every time he is tired, bored, angry, lonely, or standing near a checkout button.

The other says, “We cannot afford that,” even when the honest sentence is, “Spending money frightens me.”

| Balanced use of money | Money taking control |

|---|---|

| Saving creates margin and options | Saving becomes an attempt to eliminate all uncertainty |

| Spending supports a clear purpose | Spending manages mood, ego, boredom, or status |

| A budget reflects actual priorities | A budget becomes either punishment or fiction |

| Generosity respects real obligations | Generosity is used to buy admiration or avoid guilt |

| Frugality considers long-term value | Cheapness considers only today’s price |

| A missed goal leads to adjustment | A mistake leads to shame, secrecy, or denial |

| Money supports relationships | Money becomes a constant source of control and tension |

Financial maturity does not require one extreme to defeat the other.

It requires a better center.

Reckless Spending Is Not Living

“Do not forget to live” is not permission to spend like a raccoon found a credit card.

A man is not living well because he upgrades every device, buys every toy, eats out every night, leases more truck than he needs, and treats packages on the porch like emotional support animals.

That is not freedom. It is leakage.

Impulse spending borrows satisfaction from the future and sends the future the bill. It creates pressure, reduces options, and makes a man more dependent on overtime, creditors, luck, denial, or work he would otherwise be able to leave.

A grown man should learn to recognize mood purchases. The little voice saying, “You deserve this,” may be telling the truth. It may also be the opening line of a financial hostage situation.

Debt matters because it commits future income before the future arrives. A man should be careful about spending future freedom on temporary relief.

Saving matters because future you is not a stranger. He is you with older knees, less time to recover, and probably a much stronger opinion about mattresses.

Never Spending Is Not Wisdom Either

The opposite error looks more respectable.

A man saves, avoids debt, tracks spending, delays gratification, and builds margin. Those are good habits.

Then saving becomes a locked door.

Every invitation feels irresponsible. Every trip is too expensive. Every hobby requires a legal defense. Every repair is delayed. Every gift is too much. Every present pleasure gets cross-examined by future fear.

This can look mature from the outside. It can feel morally superior from the inside.

It can also quietly starve a life.

A man can have money in the bank and still live as though the bank owns him. He can become financially secure and emotionally cramped. He can protect the future so aggressively that the people around him stop suggesting anything that might cost money.

That is not freedom either.

Discipline becomes punishment when pain and deprivation become proof of seriousness. Money discipline can make the same mistake.

Some Opportunities Expire

This is the part many men understand too late.

Some opportunities expire.

The trip with the children expires. One day they are grown, busy, gone, or bringing their own children and looking at you the way you once looked at your parents.

The weekend with old friends expires. People move, get sick, change, or die. Some friendships do not end in conflict. They simply miss enough chances that the bridge goes quiet.

The visit with an aging parent expires. Sometimes the person is still present, but the version of them who could make the trip, hold the conversation, or remember the story is not.

The hobby expires. Bodies change. Eyesight, joints, balance, energy, and patience eventually begin submitting their own budget proposals.

A man should not use mortality to justify panic spending. “Someday we die” is not a useful budget category.

But he should let it sober him.

The future matters. So does the present. A balanced man saves for later without pretending later is guaranteed.

Spending Can Be Mature

Spending is not automatically a failure of discipline.

A mature man spends on purpose.

Protection

Some spending prevents larger problems. Maintenance, medical care, dental work, reliable transportation, safe equipment, home repairs, and appropriate insurance may feel expensive today because neglect has not yet sent its invoice.

Emergency savings exist so ordinary trouble does not become financial panic. But having money available and refusing to use it for an actual emergency defeats the point.

Time

A man may spend to buy back time. Hiring help is not automatically weakness or laziness. Sometimes paying someone with the right tools and experience protects a weekend, a marriage, a back, and the remains of a friendship that was about to be tested by plumbing.

Connection

Meals, trips, visits, date nights, shared hobbies, and family experiences can be legitimate uses of money. They do not all need to be luxurious or frequent. They need to be meaningful enough to justify the cost and responsible enough not to create a new problem afterward.

Health and Growth

Better food, decent shoes, medical appointments, therapy, a class, a book, gym access, tools, training, or equipment that keeps a man healthier and more capable can be mature spending.

Money should sometimes make a man more useful, not merely more comfortable.

Cheap and Wise Are Not the Same

A wise man looks for value.

A cheap man looks only at price.

The cheap man buys the tool that breaks and then buys it again. The wise man buys the tool that fits the need.

The cheap man delays maintenance until the repair becomes expensive. The wise man understands that prevention is often less costly than pride.

The cheap man destroys a weekend and half his lower back to avoid paying for help. The wise man knows when frugality has crossed into foolishness.

The cheap man makes every shared experience feel like an argument. The wise man protects the budget without draining the room.

Living within your means should create stability without making life unnecessarily small. The goal is not to spend the least possible amount. It is to use limited resources well.

The Question of Enough

A man who never asks “What is enough?” may spend forever.

He may also save forever.

Enough house. Enough truck. Enough tools. Enough restaurant spending. Enough emergency fund. Enough retirement contribution. Enough sacrifice. Enough delay. Enough comfort. Enough caution.

The answer changes by season, income, debt, age, health, family responsibility, and risk. But the question matters.

Without an honest definition of enough, money becomes endless hunger or endless fear. There is always more to buy, more to save, more to protect, and more to prove.

A balanced man may decide:

- We need to save aggressively this year.

- We can afford one meaningful trip, not three.

- The repair comes before the upgrade.

- We are eating out too often.

- We have been too tight and need to make some room for life.

- We can help, but not at the cost of our own stability.

- We need to spend the money because delaying this is making the problem worse.

That is adult money talk.

Not glamorous. Useful.

Build a Budget for a Life

A budget should answer more than, “How do we avoid disaster?”

That is an important question. It is not the only one.

A useful budget should reflect the life a man is trying to protect. It should address obligations, debt, risk, maintenance, future goals, generosity, relationships, health, and some reasonable amount of ordinary living.

Start with truth rather than shame.

- Look at actual spending. Review a recent month without explaining every number away.

- Protect the foundation. Cover housing, food, utilities, transportation, insurance, debt obligations, and other essentials first.

- Build margin. Create an emergency reserve and prepare for known irregular expenses.

- Name the future goals. Retirement, debt reduction, repairs, education, travel, or a job change need actual numbers rather than vague hopes. A financial goal becomes real when it has a cost, a timeline, and a plan.

- Allow responsible life now. Include an amount for meals, hobbies, trips, gifts, or experiences that fit the actual financial situation.

- Cut what adds little. Remove subscriptions, habits, impulse spending, status purchases, and recurring expenses that do not support the life being built.

- Make one correction at a time. Sustainable progress is usually less dramatic than financial panic and more effective.

The goal is not financial perfection.

The goal is a healthier relationship with money.

When Money Is Genuinely Tight

Balance does not mean pretending every household has plenty of room.

Some seasons are genuinely hard. Income may be too low. Debt may be heavy. A medical problem, layoff, divorce, repair, caregiving responsibility, or earlier mistake may consume nearly every available dollar.

A man in that season may need to say no often. He may need to delay travel, hobbies, upgrades, and comfort. Sacrifice is not automatically imbalance.

The important distinction is whether the sacrifice has a purpose and whether the plan is honest.

“We cannot afford this right now” may be the mature answer.

But even in a tight season, life cannot become nothing but punishment. Connection, rest, laughter, conversation, walks, shared meals at home, and small forms of enjoyment do not all require large amounts of money.

A man should not add financial shame to financial difficulty. Shame makes men hide numbers, avoid conversations, make desperate corrections, and build elaborate systems that last until the second weekend.

Start with what is true. Then make the next useful decision.

A Better Standard

Save money.

Save for emergencies, repairs, age, freedom, and the ability to survive an unexpected bill without turning it into a five-act tragedy.

Spend carefully.

Spend on health, protection, connection, useful tools, meaningful experiences, and the parts of life that should not be postponed forever.

Stop spending on things that mainly numb, impress, decorate, distract, or delay.

Stop saving in a way that makes life smaller than it needs to be.

Be frugal without becoming cold. Be generous without becoming foolish. Plan without worshipping certainty. Enjoy without abandoning responsibility.

Money is not the enemy.

Money is not the god.

It is a tool.

Use it like one.

Continue Building Balanced Strength

- Tenet 1: Strength Through Balance

- Consistency Beats Motivation Every Time

- When a Good Thing Becomes a God

- Discipline Without Joy Is Just Punishment

- Train for the Life You Actually Live

- Responsibility Without Resentment

- Emotional Control Without Emotional Starvation